What comes to mind when you think of investing? Not so long ago, the likely answer was stocks and bonds, maybe gold. In recent years, several alternative investment classes have caught the limelight, with Venture Capital being top of the list.

Consequently, a unicorn is no longer just a mythical creature but synonymous with a start-up company with a valuation above $1 billion – a Unicorn Company.

There are even Decacorns, start-ups above $10 billion. Ironically, Unicorn companies are not so rare as the name alludes to. CB Insights identified 1,170 unicorns worldwide as of June 2022.

However, developed market equities have had their worst first half in over 50 years. This year, government bonds have also been hit, failing to provide the protection investors usually require from them. Global stock markets are the biggest casualty of the recent turbulence, falling 15.7% in the three months to 30 June 2022. To put this into context, that’s the eighth biggest quarterly fall in the last 50 years.

With all its volatility, does this mean investors should put aside traditional investments? Should investors not focus more on venture capital where the returns seemingly lie? Let us try to unpack this question and leave you to make your own conclusion.

Venture Capital is about supporting the most ground-breaking, transformative concepts in their journey from an idea to a successful business; venture capital involves taking risks. A golden era of invention has resulted from this, and numerous new trends are forming. This has led to the emergence of a sizable number of businesses that require funding and assistance to take an idea and turn it into a successful enterprise.

Venture capital (VC) is a type of private equity that provides funding for early-stage start-ups and developing businesses with little to no operating history but high growth potential. In exchange for funding, managerial experience, and technical help, start-up businesses sell ownership holdings to venture capital funds.

Investment decisions involving securities or buying established businesses are typically made following well-known financial models, in contrast, to venture capital investing, which differs significantly. There is considerable uncertainty and danger of failure when investing in new businesses. The success of venture capital portfolios and the results of new companies are highly variable in venture capital investing.

Only accredited and institutional investors typically have access to venture capital. High-net-worth individuals (HNWIs), large financial institutions, pension funds, and wealth managers frequently invest in VC firms. Accredited Investors are people with a net worth above $1 million (excluding the value of their home) and an annual income above $200,000 (or $300,000 as a couple). The accreditation threshold exists to protect investors.

A venture capital fund makes multiple investments in a stable of promising businesses. Intending to raise the value of their portfolio firms, they frequently acquire minority holdings of less than 50%. The portfolio firm might be sold to another publicly-traded company or made public as exit plans. A secondary market sale of portfolio company shares is another option for the VC firm.

By charging management and performance fees, venture capital funds make money. The two-and-twenty fee structure is the most typical. Under this arrangement, a venture capital firm will charge its investors a management fee of 2% of the total assets under management (AUM) and a performance fee of 20% of the company’s earnings.

Risks Associated with Venture Capital Investments

Liquidity and Investment Cycle

If a corporation’s securities are “illiquid,” investors cannot sell the securities they own in that company to withdraw their money from the investment at any time, even if they do so at a loss. They need to either wait for a “liquidity event” (i.e. IPO or sale of business) or try to find a potential buyer on their own. Due to this, it carries a higher risk than traditional investments in publicly traded securities like traded equities, registered mutual funds, or other investments with a ready market for the products.

The average venture fund invests all of its capital over 10 years before returning any gains to its investors. Although there are some outliers, the 10-year life cycle is generally accepted. By mutual agreement, many 10-year funds are ultimately prolonged by 2–3 years to consolidate and disperse the final portfolio assets.

Certain future aspects become uncertain after such a long investment cycle. Barriers imposed by the government can be predictable or unpredictable. Unexpected obstacles that VCs face include economic variables like a recession or a government shutdown. Other challenges to success that raise investment risk include corporate theft of intellectual property and patent infringements.

Diversification and Risk Dispersion

You almost certainly won’t make any money if you invest in just one or a few venture capital stage businesses. Almost always, putting all your eggs in one basket is not a good idea.

Venture capital fund managers aim for success to failure ratio of 2 out of 10. This means that 2 out of the 10 investments they make must be successful. These investments need to yield 20 to 30x exit multiples for the fund to hit target returns, but returns do not come close in many cases.

How broad is adequate diversification?

In public equities, reasonable diversification can be achieved with 40 to 70 stocks. Still, one must consider factors like geographic risk and sector when constructing the portfolio.

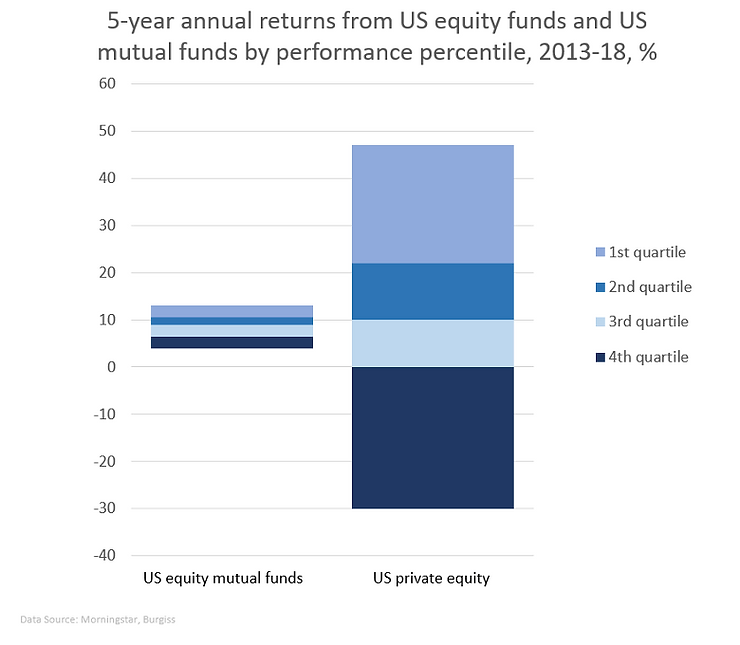

If a venture capital fund typically were to invest in 15 to 20 companies, one would need to invest in at least 3 separate funds to reach an acceptable level of diversification. Furthermore, the above chart illustrates the level of risk dispersion in the private equity asset class compared to public markets. Therefore, picking the winners and genuinely outperforming the market returns adds another factor to the equation when creating the portfolio. A track record is a significant factor in selecting funds.

Recall that one needs to be an accredited investor. Therefore, significant capital allocation from the portfolio would be required to reach the necessary level of diversification.

Venture Capital Return Compared to Other Asset Classes

Source Morningstar and Levantine & Co

Venture Capital and Private Equity have typically yielded higher than other major asset classes. That said, it is challenging to calculate private equity profits. The internal rate of return used by private equity funds to calculate returns typically considers intermediate cash flows and the fund’s initial and ending values. This can assume investors can reinvest any interim cash flows at the same rate of return, which is an assumption. Internal rate of return calculations does not have a single standard calculation method, unlike total-return calculations that must adhere to international criteria for investment performance.

Conclusion

Venture capital undoubtedly plays an essential role for accredited and institutional investors looking for long-term returns. These investors can develop highly diversified portfolios, including preferred sectors like medical industry innovation or mobility.

In recent years institutional investors have piled capital into venture capital investment. Even so, they only make a small portion of their total portfolio size. Though sometimes considered a separate asset class, all types of private equity, including venture capital, are a type of equity investment and add to the investors’ equity asset allocation. The total portfolio may also include direct investments (e.g. renewable energy investments yield predictable returns), fixed income and cash.

Ultimately, for now, a well-diversified venture capital investment portfolio remains outside the average investor’s realm. That said, investors can still reach similar risk-adjusted returns with well-managed and diversified portfolios in public securities.

If you’d like to talk to us about this, please setup an online meeting or contact us directly.